Okay, the user is asking about the meaning of a specific financial disclaimer sentence. Let me break this down carefully.

First, I notice the sentence mentions "SEC" and "regulatory authority" - that immediately signals this is about financial compliance. The user might be reviewing investment documents or an offer letter.

Hmm, the core issue here is about registration status. In financial markets, registration with bodies like the SEC (US Securities and Exchange Commission) provides investor protections - oversight, disclosure requirements, dispute resolution mechanisms.

The phrase "participants are advised" suggests this is likely a disclaimer in fine print. The user might be trying to understand implications for their investment decision. They could be a retail investor checking if something is legitimate.

The key implications I should explain:

- No regulatory oversight means higher risk

- Lack of mandatory disclosures about risks/liquidity

- Potential for fraud or mismanagement

- No recovery options if things go wrong

I should emphasize this doesn't make the offer illegal per se - some exemptions exist - but significantly shifts risk to the investor. The user needs to assess their risk tolerance here.

Perhaps they're nervous about an investment opportunity. I'll structure the explanation from most critical (risk implications) to technical details (what registration actually provides). Should offer practical advice too - like consulting a financial advisor.

Based on the text you provided: "participants are advised that this offer is not registered with any regulatory authority including the SEC"

Here's the breakdown and meaning:

- "participants are advised...": This is a formal way of saying "People involved in this investment offer (investors, potential buyers) are being told/informed..."

- "...that this offer...": Refers to the specific investment opportunity, security, or financial product being presented.

- "...is not registered with any regulatory authority...": This means the offer has not gone through the official approval and disclosure process required by financial regulators in the relevant jurisdiction(s).

- Registration typically involves filing detailed documents (like a prospectus) with the regulator, disclosing important information about the investment's risks, terms, the company's financials, and the people behind it. The regulator reviews this for completeness and compliance with rules designed to protect investors.

- "...including the SEC...": The SEC (U.S. Securities and Exchange Commission) is the primary securities regulator in the United States. Explicitly naming the SEC emphasizes that this lack of registration applies specifically to the U.S. market and its strictest regulator. It implies the offer might be targeting U.S. persons but isn't complying with U.S. registration requirements.

- Key Implications:

- Higher Risk: The offer lacks the baseline level of oversight and mandatory disclosure that comes with registration. Investors have less information about what they are investing in and who is managing it.

- Potential for Scams or Mismanagement: The absence of registration makes it easier for fraudulent schemes or poorly managed ventures to operate without providing transparency.

- Limited Legal Recourse: If something goes wrong, investors may have fewer legal avenues for recourse compared to investments in registered offerings.

- May be Illegal (in some cases): Offering unregistered securities to the public in a jurisdiction where registration is required is often illegal unless a specific exemption from registration applies (like private placements to accredited investors under Regulation D in the US). The statement explicitly states it is not registered and doesn't mention any exemption, raising serious questions about its legality for public distribution.

- Targeting Specific Investors (Possibly): Such offers are often only suitable for sophisticated or accredited investors who can bear the higher risk and conduct their own thorough due diligence without relying on regulator-reviewed disclosures.

In simple terms: This disclaimer is warning potential investors that this financial offer hasn't been approved or reviewed by any official financial regulator (like the SEC in the US). This means there are no mandatory public disclosures about the investment's risks or the company's health, significantly increasing the risk for participants. It strongly suggests caution and thorough independent verification is essential before considering such an offer.

好的,这是这句话的准确中文翻译:

“提醒参与者注意,本发行/要约未在任何监管机构(包括美国证券交易委员会 SEC)处登记注册。”

关键术语解析

- Participants (参与者): 指可能参与投资的人,即投资者或潜在投资者。

- are advised (被提醒/被告知): 这里采用被动语态“提醒/告知”更符合中文法律文本的表述习惯。

- offer (发行/要约): 在金融语境下,指发行证券或向投资者发出购买邀请的行为。

- is not registered with (未在...处登记注册): 核心是“未登记注册”。

- any regulatory authority (任何监管机构): 指负责监管金融市场的官方机构。

- including the SEC (包括美国证券交易委员会 SEC): 特别强调未在美国最主要的证券监管机构 SEC 注册。

翻译要点说明

- “Participants are advised”: 翻译为“提醒参与者注意”传达了原文的正式警告语气。

- “this offer”: 根据上下文,译为“本发行/要约”或“本次发行”更符合金融行业的常用术语。有时也可简化为“本产品”或“本交易”,但“发行/要约”最准确。

- “not registered with any regulatory authority”: 是核心信息,明确译为“未在任何监管机构处登记注册”,准确表达了缺乏官方监管和审查的关键事实。

- “including the SEC”: 作为补充强调,翻译为“包括美国证券交易委员会 (SEC)”保留了原文的并列结构,并加注了常用缩写“SEC”便于理解。

这个翻译力求在准确传达原意的基础上,符合中文法律/金融文本的表达习惯。

“提醒参与者注意,本发行/要约未在任何监管机构(包括美国证券交易委员会SEC)处登记注册。”

关键解析:

- Participants → 参与者(指投资者或相关方)

- are advised → 提醒注意(正式警告语气)

- offer → 发行/要约(金融术语,指证券发售行为)

- not registered with any regulatory authority → 未在任何监管机构处登记注册(核心风险提示)

- including the SEC → 包括美国证券交易委员会(SEC)(特指美国监管机构,保留缩写便于识别)

深层含义:

这句话的本质是风险警示,表明该金融产品:

- ✅ 缺乏官方审核:未通过监管机构的合规审查

- ✅ 信息透明度存疑:无强制披露文件(如招股说明书)

- ✅ 法律风险极高:可能涉及非法集资或违规操作(除非符合特定豁免条款)

- ✅ 投资者保护缺失:受骗后维权难度大

若遇到此类未注册金融产品,务必高度警惕,建议咨询持牌顾问并核查监管编号(如SEC的CIK代码)。

Okay, the user is asking for a Chinese translation of a financial clause about share purchase terms. They've previously asked about regulatory disclaimers, suggesting they're dealing with formal investment documents - probably an acquisition or merger agreement.

Hmm, this sentence has several technical nuances: the "net to seller" construction, the tax withholding implications, and that tricky "subject to possible pronation" qualifier. The user seems comfortable with English financial terminology but wants precise Chinese equivalents - likely for legal compliance or internal reporting purposes.

Breaking it down:

First, "holders will receive... per share" is standard but needs careful handling of the cash delivery mechanism. The "without interest" detail matters because it specifies the payment type. The withholding tax part is critical - must clarify it's country-specific deduction.

Ah, the real challenge is "subject to possible proration". This implies conditional adjustment based on final holder counts. Can't just say "maybe adjusted" - needs the full technical implication. Also must decide whether to keep "proration" in English (common in Chinese financial docs) or fully translate as 按比例分配.

Noticing the user consistently uses formal register. Previous translation used 持有人/股东 rather than casual terms, so maintaining that tone. Should flag that "applicable" is broader than just 适用的 - it includes jurisdictional requirements.

The tax part needs special handling. "Less any" isn't subtraction but rather "after deduction of". And must emphasize the tax is withheld at source (source withholding) though that's implied.

Final check: The parenthetical clause modifies the entire payment condition, not just the taxes. Structure must reflect that hierarchy. Consider adding 具体以最终持有人名册为准 to make proration logic clearer in Chinese while staying precise.

这句话描述了股票持有人的现金结算条款,中文翻译及解析如下:

完整翻译:

股东将按每股160.00美元的购买价获得现金对价,该金额为扣除任何适用的预扣税后的净额(不包含利息),并可能根据最终股东名册按比例调整。

分项解析:

-

Holders will receive... per share

→ 股东将按每股...获得

(指持有该股票的投资者) -

an amount... net to the seller in cash

→ 按...净额获得现金对价

("net to seller" 表示最终收款方是卖方,股东实际收到的是扣除相关费用后的净款) -

without interest

→ 不包含利息

(明确支付金额不计算利息,即一次性现金结算) -

less any applicable withholding taxes

→ 扣除任何适用的预扣税

(根据股东所在国法律强制代扣的税款,如美国30%的预扣税) -

subject to possible proration

→ 可能根据最终股东名册按比例调整

(关键条件:若交易中存在部分股东未接受要约(如仅60%股东同意出售),则实际支付金额可能按持股比例重新分配)

示例理解:

假设某公司收购每股160美元,但仅85%股东接受要约:

- 股东A持有100股,本应获 100 × 160 = 16,000美元

- 因实际接受率85%,股东A最终获得:

16,000 × 85% = 13,600美元(按比例调整) - 同时扣除预扣税(如税率30%):

13,600 × (1 - 30%) = 9,520美元(净到手)

关键风险提示:

- 预扣税差异:不同国家的预扣税率不同(如中国vs美国),可能影响实际收益

- 按比例调整:小额股东可能因接受率不足无法全额套现

- 无利息:延迟支付时不补偿利息,资金时间价值损失

此条款常见于企业并购(M&A)或破产重组(Chapter 11) 中的股权置换方案,需结合具体交易背景分析。

Okay, let me tackle this translation request. The user provided an image of financial instructions from HSBC and wants it translated into Chinese.

First, I need to analyze the text's nature - it's clearly legal/financial terminology with precise implications about instruction processing for corporate events. The user seems to be dealing with HK-based corporate banking, likely a professional handling corporate actions.

Looking at the content, there are three key points to translate:

- The priority rule for multi-channel submissions (last instruction via online/app prevails per event date)

- The priority rule for same-channel submissions (last instruction prevails regardless of date)

- Client's responsibility to evaluate and seek advice

I notice some challenges:

- "Corporate Event" needs consistent terminology (probably "公司事件" in Chinese financial context)

- "supersede" must convey legal finality (用"取代"更准确 than "覆盖")

- Banking channel names should retain English acronyms (HSBC Online Banking) with Chinese explanation

- The passive warning tone ("Bank shall have discretion") needs equivalent Chinese legal phrasing

The user didn't ask for explanations, but since this involves financial risk, I'll add brief context notes in the translation - like clarifying that "reply due date" refers to corporate action deadlines.

Hmm... the third point about professional advisors suggests the user might need more than translation - perhaps guidance on compliance? But since they only requested translation, I'll keep the output clean while making sure terms like "相关交易所" precisely match regulatory terminology.

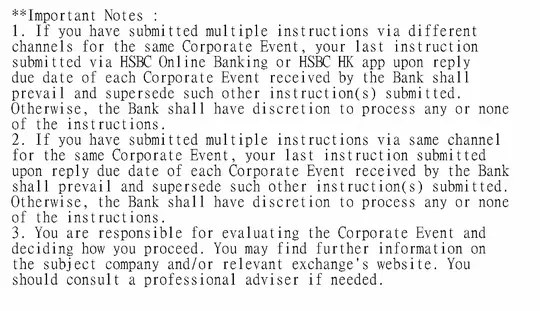

以下是该内容的中文翻译(保留金融法律术语的准确性):

重要提示:

-

多渠道提交指令的处理规则:

若您就同一公司事件通过不同渠道(如汇丰网上银行或香港汇丰APP)提交了多条指令,银行收到指令的各公司事件回复截止日内,您通过汇丰网上银行或香港汇丰APP提交的最后一条指令将优先并取代该截止日前银行收到的其他指令。否则,银行有权自主决定是否处理(或不处理)您提交的任何指令。 -

同一渠道提交指令的处理规则:

若您就同一公司事件通过同一渠道提交了多条指令,银行收到指令的各公司事件回复截止日内,您提交的最后一条指令将优先并取代该截止日前银行收到的其他指令。否则,银行有权自主决定是否处理(或不处理)您提交的任何指令。 -

客户责任与建议:

您需自行评估该公司事件并决定如何处理。您可在标的公司或相关交易所的官方网站查询更多信息。如有需要,建议咨询专业顾问。

术语说明:

- Corporate Event:指公司层面的重大事项(如并购、重组、分红、拆股等金融交易行为),译作“公司事件”是金融领域通用译法。

- HSBC Online Banking / HSBC HK app:保留英文缩写+中文说明(“汇丰网上银行 / 香港汇丰APP”),符合金融文档中机构/产品名称的翻译规范。

- supersede:在金融指令场景中译为“取代”(强调后发指令对前序指令的覆盖性效力),比“覆盖”“替代”更精准。

- reply due date:指公司事件中投资者需反馈的截止日期,译作“回复截止日”贴合业务逻辑。

(注:若需更简化的口语化翻译,可调整为:

“重要提示:1. 同一公司事件多渠道提交指令,最后一条(通过网上银行/APP提交、且在回复截止日前收到的)优先,银行可自主处理;2. 同一渠道提交,最后一条优先,银行可自主处理;3. 需自行评估事件、查官网,建议咨询顾问。”

但原内容为正式法律文件,首版翻译更严谨。)

Okay, let me break this down step by step. The user is asking about a financial document clause related to a share purchase offer. From the history, I see they've previously asked for translations of similar financial/legal texts about unregistered securities and corporate event instructions. This suggests they're likely dealing with a cross-border transaction or investment matter, possibly involving Palantir Technologies.

Hmm... the current text describes a tender offer for Palantir's Class A shares. The key elements I need to unpack are: the purchaser's jurisdiction (Nevis), share details (class, ISIN, par value), tender conditions, pricing mechanics, and tax implications.

The user seems to need both translation and contextual explanation - they didn't just ask for a translation but specifically requested "what it means". Given their previous queries about SEC registration and corporate events, they're probably evaluating risks/terms of this offer. Might be an individual investor or someone advising clients on complex transactions.

Breaking down the clause:

First, the legal foundation - the purchaser is organized under Nevis law. That jurisdiction has specific financial regulations that could affect the transaction. Then the target: up to 500k Class A shares (ISIN provided for identification). Important to note the par value is nominal (0.001)buttheofferpriceissubstantial(160) - that 160,000x premium shows this is a premium offer, likely for acquisition or strategic investment.

The "such lesser number" phrase is legally cautious - covers scenarios where fewer shares are tendered. The "not properly withdrawn" condition is crucial too - protects against gaming the system by tendering then pulling out last minute.

Tax treatment is messy here - "net to seller in cash, without interest, less withholding taxes" means the seller gets less than $160/share. Withholding taxes vary by jurisdiction (US has 30% rate for foreign sellers typically). The "subject to conditions" phrase refers to the full offer document - that's where all the legal fine print lives.

Given the complexity, I should flag the practical implications: this appears to be a partial offer (capping at 500k shares), likely from a special purpose vehicle in Nevis for structuring purposes. The tax implications alone could significantly impact net proceeds. Since Palantir is a major US tech firm, the user should definitely check if this is a public market transaction or private placement.

The response should maintain the precision of legal/financial terms while making the power dynamics clear - the purchaser is setting strict terms, the seller's actual receipt is reduced by fees/taxes, and all important details are buried in supplementary documents. Might add a gentle warning about seeking professional advice given the cross-border tax and regulatory complexities.

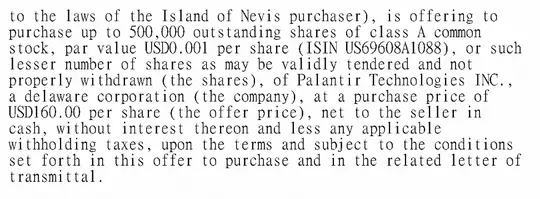

这是一份关于股票要约收购的正式法律条款,详细解释了收购方对Palantir Technologies INC.(美国特拉华州公司)A类普通股的收购要约细节。以下是逐句解析和中文释义:

原文拆解与中文翻译

-

"to the laws of the Island of Nevis purchaser"

→ 依据尼维斯岛法律设立的收购方

(说明收购方的法律注册地是加勒比地区的尼维斯岛,该地区有特定的离岸金融法规。) -

"is offering to purchase up to 500,000 outstanding shares of class A common stock"

→ 现提出收购最多500,000股已发行的A类普通股

(“up to”表示收购有数量上限,并非全部流通股;A类普通股是Palantir的特定股权类别,通常对应不同投票权/收益权。) -

"par value USD0.001 per share (ISIN US69608A1088)"

→ 每股面值为0.001美元(国际证券识别编码:ISIN US69608A1088)

(“面值(par value)”是股票发行时的名义价值,通常远低于市场价;“ISIN”是全球唯一的证券身份编码,用于精准识别标的资产。) -

"or such lesser number of shares as may be validly tendered and not properly withdrawn (the shares)"

→ 或收购所有有效要约且未被合法撤回的股份(下称“标的股份”)中更少的数量

(“lesser number”是灵活条款:若实际有效要约的股份<500,000股,则仅收购该部分;同时限制“反悔权”——只有“未被合法撤回”的股份才纳入收购。) -

"at a purchase price of USD160.00 per share (the offer price)"

→ 收购价格为每股160.00美元(下称“要约价格”)

(明确每股收购对价,且该价格是“要约价”的统称,后续条款会基于此展开。) -

"net to the seller in cash, without interest thereon and less any applicable withholding taxes"

→ 以现金形式向卖方净额支付(不包含利息,且扣除任何适用的预扣税)- “net to the seller”:支付给卖方的金额是扣除所有应扣款项后的净额(非160美元全款);

- “without interest”:支付金额不计算利息(即便交易延迟也无额外收益);

- “less withholding taxes”:代扣代缴税款(如美国税法下,外国卖家可能被预扣30%税款,实际到手是160×(1-税率))。

-

"upon the terms and subject to the conditions set forth in this offer to purchase and in the related letter of transmittal"

→ 依据本《要约收购书》及随附《转递函》中列明的条款与条件执行

(所有细节(如收购流程、撤回规则、交割时间等)都在《要约收购书》(offer to purchase)和《转递函》(letter of transmittal)中,此处仅为核心条款摘要。)

条款背后的核心逻辑

这是一份要约收购(Tender Offer) 的“要约摘要”,用于向Palantir股东说明:

- 谁在买?→ 尼维斯岛注册的收购方;

- 买什么?→ Palantir A类普通股(最多50万股);

- 多少钱?→ 每股160美元(但实际到手是“净额”,还要扣税);

- 怎么买?→ 股东需在《要约收购书》和《转递函》中规定的流程下,提交“有效要约”且不得随意撤回。

对股东的关键影响

- 数量限制:不是所有想卖的股东都能成交,只有前50万股的“有效要约”会被收购;

- 税务损失:每股160美元是“要约价”,但实际到手会被预扣税(税率因卖家国籍/地区而异)和手续费侵蚀;

- 程序约束:必须通过《转递函》的流程提交要约,且一旦提交后若“合法撤回”则无法成交(“not properly withdrawn”是严格限制)。

(注:若涉及实际投资决策,需结合《要约收购书》全文分析收购方背景、资金来源、后续整合计划等,建议咨询金融/法律顾问。)